The UK market for domestic garden buildings and structures has seen slow but steady growth in recent years. The overall sector is mature and highly dependent on replacement purchases as well as consumer confidence levels.

Improving consumer confidence and spending in 2014 and 2015 stimulated demand for all product groups resulting in annual growth rates of around 3% per year, but whilst growth has continued since, more modest rates have been achieved more recently and the market increased by only 1% in 2017, in value terms.

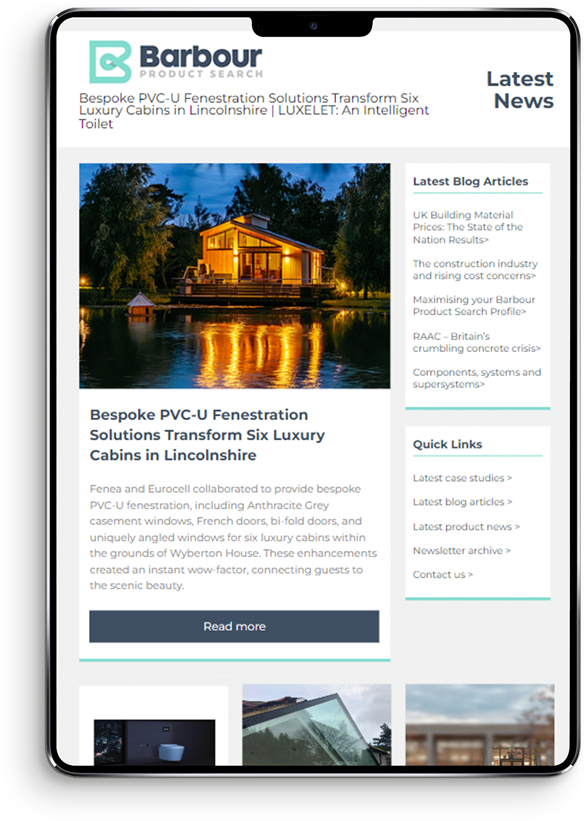

Within the domestic garden buildings market, there are sectors that are mature and established, such as sheds and greenhouses, but also sectors that are less mature, such as garden rooms. Household ownership of ‘buildings for all year-round use’ is very low. These types of buildings are used for a variety of purposes such homeworking, leisure activities and accommodation, something which has helped to increase demand for higher specification buildings, boosting market value.

As is the case with most garden related products, the weather impacts directly on market performance, although some sectors are more vulnerable to fluctuations in the weather than others. Summerhouse sales, for example, are very seasonal, while log cabins and garden rooms are less so. In some cases, poor weather conditions can also temporarily boost sales. Stormy weather can cause damage to buildings and structures, and has the potential to stimulate demand for replacement products and, in some cases, more robust alternatives.

Within the overall domestic garden buildings market, there have been significant differences in performance between sub-sectors. Sheds and garden storage, the largest sub-sector, accounts for around one third of the market and remains a stable sector. Growth has been particularly strong for metal and plastic sheds & storage, in part be due to the increasing cost of timber.

While demand for log cabins has fallen in volume terms, the sector has benefited from a degree of upgrading and price increases. The summerhouses sector has been static and is experiencing increased competition from other product sectors, such as garden structures. Garden buildings for all year use represent a similar but slightly smaller share than log cabins and summerhouses. This sub-sector continues to see an increase in the cost of the average unit, due to an increase in specification and size of unit, improving market size.

Greenhouses and garden structures are the two smallest sub-sectors, with garden structures only representing around 3% of the overall market.

Key distribution channels for products such as summerhouses, sheds, greenhouses and garden structures at the lower end of the market, are the home improvement multiples and online/mail order companies. In contrast, higher value products, such as modular garden rooms and timber framed buildings, are generally sold direct to the customer, the majority with services such as installation included, although some are sold as self-assembly. An increasing number of manufacturers are also selling via their own websites.

Prospects for the overall garden buildings and structures market into the medium-term remain relatively optimistic with the market forecast to see steady growth rates of 2-3% per year until 2022. Consumer confidence and spending has started to show signs of deterioration and may impact on market development going forward, while other influencing factors include housebuilding & house moving levels, design trends, product specifications and product developments.

The 'Domestic Garden Buildings and Structures Market Report - UK 2018-2022' is availble now and can be ordered online at www.amaresearch.co.uk or by calling 01242 235724.

Related Blog Articles

%20227.png "Maximising your Barbour Product Search Profile")