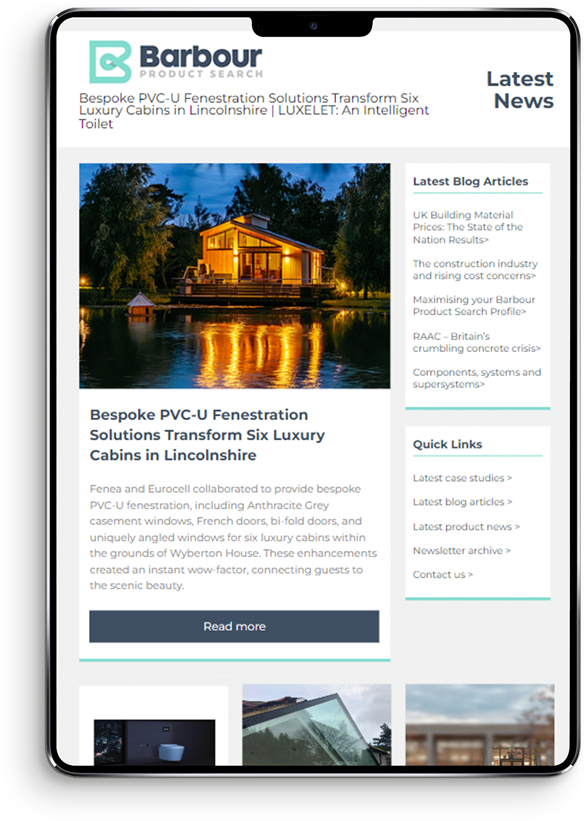

Health sector construction output peaked at £5.9bn in 2008, followed by a decline of around 50% to around £2.9bn in both 2015 and 2016 before recovering to around £3.3bn in 2018, according to the latest information from AMA Research.

Despite 4 years of declining output between 2011 and 2014, the current outlook for health construction output growth remains steady, if moderate, into the medium-term, with annual rates of growth of 3-5% currently forecast to 2021.

Output has benefited from the hospital building programme initiated by the previous government, much of which was delivered under PFI programmes. Despite a handful of large PFI hospitals still expected to complete over the next couple of years, the emphasis is now firmly on smaller acute projects through Procure21+ and Procure22 and in the primary care sector on GP surgeries/health centres through ExpressLIFT. Public sector output has however experienced fluctuations due to budget cuts impacting on the sector.

As a result of GP-led commissioning and financial constraints, the procurement of services to the NHS, including construction, are increasingly looking towards increased partnership with the private sector. A further driver is also taking place in the acute healthcare sector with the creation of NHS Foundation Trusts, under which hospitals can generate their own income. As a result, there has been a rise in private providers refurbishing part of existing hospitals, adding extensions, new-build facilities or even taking on the full operation of a hospital.

The key construction opportunities in the healthcare sector are likely to be in the primary care sector and this may entail further opportunities for the development of hub facilities and integrated GP premises, while in the acute and secondary sector, much of the medium-term is expected to lie in refurbishment and extensions.

Contractors will also be interested to see how new procurement routes and private finance initiatives, including P22, will be used to procure work in the health sector in 2017/18 and beyond, with the expiration of the Express LIFT framework and future options for health PPPs being explored.

Future prospects look relatively bright, with the Government having announced a forward pipeline of around £5.7bn worth of capital projects in the healthcare sector between 2017 and 2020, and beyond. This includes nearly 600 individual health projects under almost 100 schemes, which are mainly spread across the English regions, of which there are around 10 large NHS-led capital programmes, in addition to smaller works and capital programmes procured via the Procure 21/Procure21+ frameworks.

However, whilst the Department of Health was allocated £4.8bn for capital investment for each year to 2020-21 in the 2016 Budget, this represents a real-terms cut of 1.7% per year.

The moderate forecast of 3-5% growth per annum is based on the steady level of health sector new orders over the last 2-3 years, and the focus on delivery of local services and chronic disease prevention initiatives put forward by successive Governments.

Health RMI into the medium-term is also likely to remain positive but moderate and there are likely to be significant regional differences, especially where demand for key services is high. The focus on partnerships to drive increased efficiency and productivity, whilst lowering construction and maintenance costs is forecast to continue.

Related Blog Articles

%20227.png "Maximising your Barbour Product Search Profile")

{kind=link}